Are you a gun owner? We know that you are and we have a serious discussion for you.

Have you considered concealed carry insurance?

If not, you’re putting your family and yourself at risk. That’s right: you can legally conceal carry and still risk financial ruin and criminal charges.

You can do everything right, but without ccw insurance, you’re risking leaving your family financially unstable.

USCCA concealed carry insurance eliminates these risks.

When you have insurance, you’re doing everything right.

How Concealed Carry Insurance Works

Before discussing USCCA Insurance, all gun owners need to know how concealed carry insurance works. When you take out insurance, you’re taking out a policy that protects you if you shoot someone, with the proper concealed carry licensing, in self-defense.

The key most important word here is self-defense.

Insurance will protect you from:

- Criminal liabilities

- Civil liabilities

Think of concealed carry insurance like auto insurance. You’ll carry the insurance hoping you never need it, but if someone breaks into your home and tries to harm your family, your insurance will kick in.

Let’s say that you shoot someone in self-defense.

Perhaps the person was breaking into your home or harming your child, so you pull out your gun and shoot them. If you have a policy, you can call USCCA Insurance (there’s a hotline) and file a claim with the insurance provider.

The representative on the other line will walk you through the entire process of filing a claim.

But this is a specialized niche. There aren’t a lot of carriers, and every insurance company has their own policy limits and requirements. What’s important to know is that, just like car insurance, there are policy limitations.

You’ll find that many plans offer limits for:

- Civil / criminal defense

- Bail bonds

- Money for losses incurred during court proceedings

If you do shoot someone in self-defense and charges are pressed against you, the insurance policy will kick in, protecting you from financial hardships.

USCCA Insurance Review

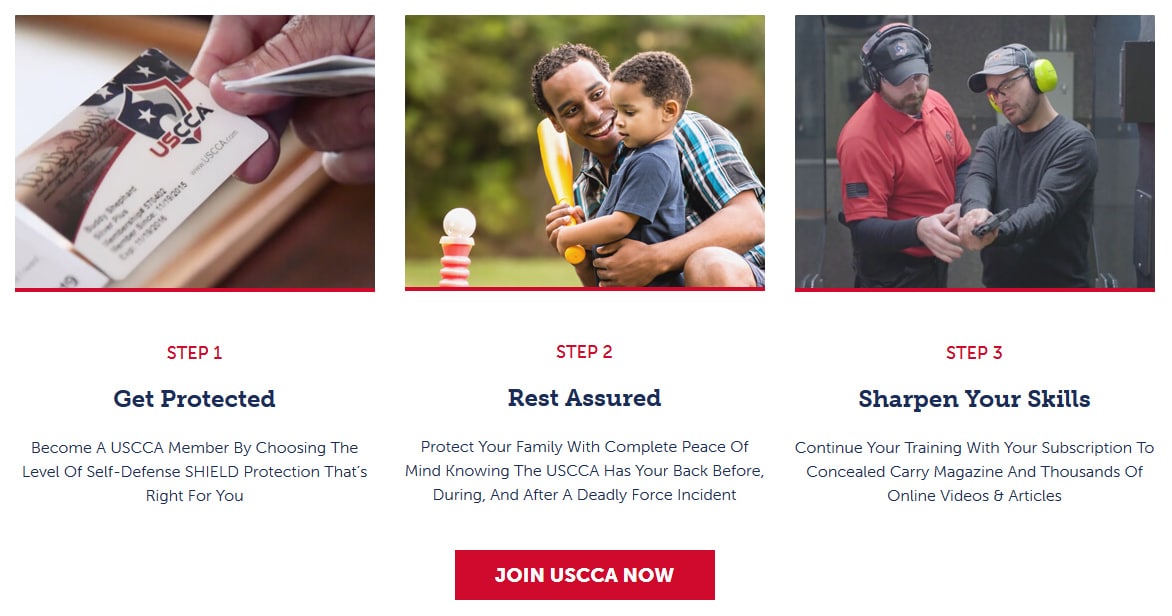

USCCA Insurance is the leader in concealed carry insurance, and it’s a company that is well-known and trusted by gun owners across the country. What’s unique about USCCA is that the company offers a three-step plan to being a confident, responsible gun owner.

First, the company offers what they call the USCCA Self-Defense SHIELD.

The SHIELD is the level of protection that’s right for you. We’ll be covering the many different shield levels shortly.

But the insurance company doesn’t just provide a policy.

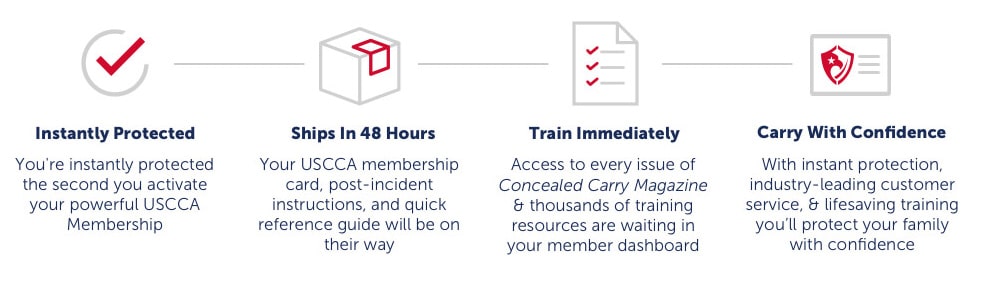

You’ll also become a member of one of the most respected communities available. You see, training is a main part of USCCA, and the company provides ways for all gun owners to start sharpening their skills.

USCCA will provide you with the following as a member:

- Thousands of videos

- Thousands of articles

- Concealed Carry Magazine subscription

As a member of USCCA, you’ll learn a lot of the laws, safety tips and information about guns that top security experts utilize. This is a membership, not just an insurance policy, that works to make you a responsible gun owner.

You’ll be shielded from financial risk when you have an annual membership.

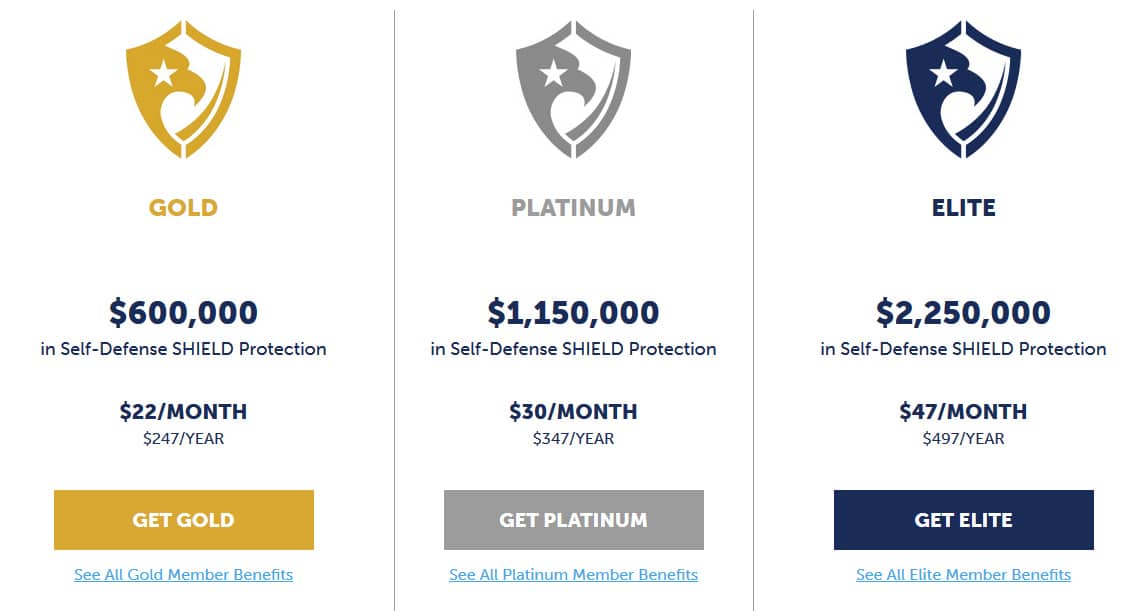

USCCA Self-Defense SHIELD Levels

Remember how we mentioned that there are three different shield levels?

Well, the shield levels available are:

- Gold

- Platinum

- Elite

And each policy will cover you in the event that you’re sued for defending yourself or your family. The main difference between all shield levels is the cost and coverage limits.

Gold – $600,000 in Protection

The Gold level is the entry-level protection. You’ll have $600,000 in self-defense protection, and your premiums will be $22 a month, or $247 if you pay yearly. When choosing the Gold level, you’ll have the following policy benefits:

- $500,000 in civil suit defense and damages coverage

- $100,000 in criminal defense protection

Criminal defense protection is key because it provides an up-front attorney retainer. You’ll be able to sleep well at night knowing that you can hire one of the best attorneys with $100,000 waiting for your defense.

But the benefits don’t stop there.

You’ll also receive the following:

- $350 per day in compensation while you’re in civil court. This means that you’ll be compensated for money you would have made at your job.

- $5,000/$50,000 for up-front bail bond funding to get you out of jail and back to your loved ones.

- $3,000 for personal hardship coverage.

- $3,000 for psychological support.

Psychological support is huge because a lot of gun owners don’t realize the stress and pressure they’ll be under if they have to use their gun in self-defense. A lot of owners will question their actions, lose sleep at night and even suffer from PTSD after shooting someone.

Psychological support can help you ease your mind and return to your old life as quickly as possible.

Platinum – $1,150,000 in Protection

Platinum protection is the next step up, and this protection offers everything that gold has to offer but at a higher limit. You’ll be paying $30 a month, or $347 for the year, but you’ll also receive:

- $1 million in civil suit defense and damages coverage

- $150,000 in criminal defense protection

- $500 per day in compensation

- $25,000/$250,000 for up-front bail bond funding

- $4,000 for personal hardship coverage

- $4,000 for psychological support

If you need even more coverage, and if you have the money I recommend it, you should move on to the final tier: Elite.

Elite- $2,250,000 in Protection

Elite protection is the best-of-the-best, and it’s the coverage that every gun owner with the finances should obtain. When you choose this coverage, you’ll spend $47 a month or $497 for the year. If you pay for the year up-front, you’ll save $100, so it’s a good deal either way.

This insurance option offers:

- $2 million in civil suit defense and damages coverage

- $250,000 in criminal defense protection

- $750 per day in compensation

- $50,000/$500,000 for up-front bail bond funding

- $6,000 for personal hardship coverage

- $6,000 for psychological support

But there are also universal membership benefits. All policyholders for USCCA Insurance will receive the following benefits as a member:

- 24/7 support from the USCCA critical response team

- No deductible / no reimbursement coverage

- No annual limits – limits are per incident

- Coverage on all weapons owned

- Attorney counseling

- Expert witness coordination

- Member discount and deals

- Local attorney coordination

- Firearm theft coverage

You’ll also receive a subscription to the Concealed Carry Magazine. Again, every SHIELD level will receive these unique benefits.

FAQ: When Choosing The Best CCW Insurance

I had a lot of questions when signing up with USCCA, so I know that it’s a difficult choice to make. A few of the questions and answers that helped to ease my mind and make my choice a bit easier were:

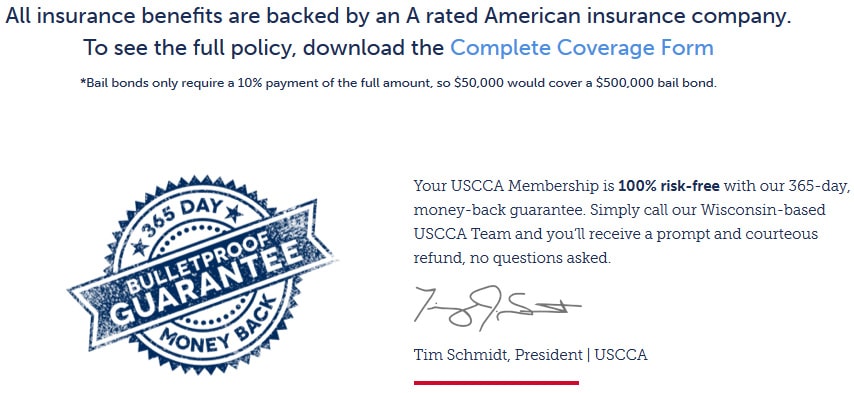

- Can I cancel my membership? What’s awesome about choosing this company is that they offer a 365-day guarantee. You’ll receive 100% of your money back, and there are no questions asked. If you don’t feel your plan is beneficial or it doesn’t meet your standards, initiate a cancellation and receive all of your money back.

- Do I receive reimbursement? You never have to pay for any of the plan’s costs aside from membership. There’s never a reason to ask about reimbursement when there’s no deductible. All of your costs are paid up-front, so you never have to suffer a financial burden.

- Will my spouse be covered? In fact, anyone in your care that is under 21 will be covered as well as your relatives. Coverage is only available on your property, so the incident must occur on your property. Spouses can receive full coverage by paying just $47 – a great deal.

- Do I need a permit? Remember, USCCA has your back. The company knows you’ll reach for the first weapon you have to defend your family. You can reach for a knife, sword, gun or any other weapon. If the act is in self-defense, you’re covered no matter what weapon you use or if you have a permit.

- Do I have to use USCCA’s attorney network? You have the opportunity to use the network, but at the end of the day, you choose your attorney. The policy will cover costs of an attorney whether or not they’re part of the company’s network.

- When will I receive Concealed Carry Magazine? Good question. I had to do some digging, but I found that it really depends on the publish date. The magazine publishes new issues every 45 days, so you may need to wait up to 45 days to receive your issue. There are 8 issues before your renewal date. The USCCA app or Membership Dashboard will provide you with online, digital access to the magazine. It’s filled with a lot of great information, so make sure to read your issues when they’re available.

Your spouse and relatives receive coverage, and any person in your care will also receive coverage if they’re under 21 – that’s impressive. The company will also be there to help you through every question you have if you need to file a claim.

Representatives are there day and night, all year long, to answer your difficult questions and help you file a claim.

What’s really nice is that you can also contact USCCA whenever you want. As the leading self defense insurance provider will be ready and waiting to answer any other questions you have. If you would rather to talk a representative online, you also have that option.

The company will answer all of your questions to the best of their ability.

For me, being able to reach out to the company and talk to someone directly is huge. Few companies offer that benefit.

What is the Best Concealed Carry Insurance?

If you want the best insurance, you’ll find two powerhouses pitted against each other: USCCA and NRA Carry Guard. Which is the better option? I go with USCCA. Here’s why:

NRA Carry Guard vs USCCA

When breaking down the coverage between both of these insurance providers, you’ll find that each has their own set of tiers. NRA has four unique tiers to pick from:

- Bronze: $13.95 per month /$154.95 annually

- Silver: $21.95 per month /$254.95 annually

- Gold: $31.95 per month /$359.95 annually

- Gold Plus: $49.95 per month /$549.95 annually

NRA doesn’t offer the steep discounts that USCCA does, and when comparing tiers, I am going to be comparing USCCA’s Platinum versus NRA’s Gold tier because they’re closest in coverage.

Price-wise, USCCA wins, with $347 vs $359.95 being the cost. Coverage is higher at $1,150,000 versus $1 million.

NRA lumps their $1 million together, while USCCA’s does not. And this is a minor coverage difference that a lot of owners could understand.

Then comes the criminal defense payment. USCCA offers 100% payment up-front. When it comes to NRA, they offer just:

- 20% up-front

- 80% if not guilty

If you’re found guilty, you’re responsible for 80% of the criminal defense costs – no thanks.

NRA covers only firearms, while USCCA covers all weapons. NRA does offer spousal coverage outside of the home while USCCA does not.

NRA Carry Guard does not have an attorney network.

So, as you can see, the coverage limits are similar, yet USCCA does offer better overall coverage. A major deciding factor for me is that the criminal defense payment is only 20% up-front with NRA.

If I am paying for a policy, I want to be fully covered.

USCCA will offer 100% up-front payment for criminal defense, and if you ask me, this is the right decision for all gun owners. You are also covering yourself for all weapons, so this is beneficial for non-firearm owners, too.

Where to Buy USCCA Insurance

I recommend buying your insurance from the company’s official website. Pay annually and you receive a discount. It’s that simple. If you’re being offered USCCA insurance from somewhere else, it’s more than likely a scam.

Remember, you can save $100 on the best plan by paying $497 for the year.

It’s a great deal.

If you’re a gun owner and will protect your family at all costs, you need USCCA Insurance.

Click here to view more information and become USCCA insured today.